The debt and saving problem in South Africa

Debt and saving are not two words that you would associate with one another. Debt is generally negative, while saving is positive and encouraged. As Stuart Theobald of Intellidex and Grant Locke of OUTvest explained in a Business Day article last week, South Africa has a problem.

“Much of the lending industry has evolved into something that harms rather than helps the financial position of the average client,” says the article. This means that many South Africa’s are in trouble and we need to change some of our habits in order to secure a better financial future.

But what does this really mean? And how has debt put South Africans on the back foot?

Simply put, we borrow more money than we save. This means “we are creating a future in which millions of South Africans will be retiring with insolvent personal balance sheets, saved from abject poverty only by meagre state pensions.” A rather bleak outlook, but we need to look back and establish how South Africa arrived in this position in order to move forward.

How have South Africans managed to get ourselves in this position?

Bad decisions and increased borrowing are at the root of the problem. This is not to say that South Africans weren’t borrowing money prior to the problem being identified. Stuart and Grant noted that, “Over the past four decades, consumer debt has shifted from largely productive borrowing that supported the accumulation of real assets, into largely unproductive financing of consumption.” This means more bills and fewer assets to show for them… a horrible spiral to be in.

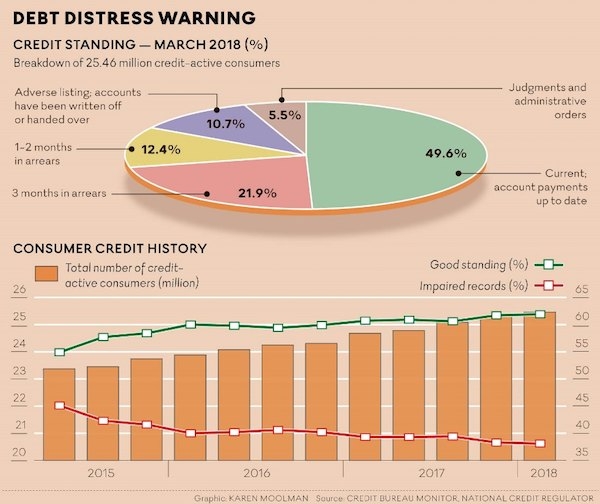

So it’s clear that as a country we have a problem. The average savings rate of disposable income is below zero and the total debt held by South Africans is above 70% of disposable income. What is the best way to go about addressing the problem?

The authors believe that “we need a financial services industry that works to improve the balance sheets of consumers”. Tax-free savings accounts, fintech offerings that increase access, and financial education will all play a role in helping South Africans to address this problem.

Read the full article on the Business Day website: Disaster awaits if the finance sector fails to give consumers a better deal.

If you would like to know about Stuart Theobald you can visit the Intellidex website. To learn more about Grant Locke and OUTvest visit their website. Stuart and Grant are both passionate about helping South Africans address this problem.

Who wants to be a millennial millionaire?

CN&CO’s Thabs Royds will be joining a panel of her fellow millennials, Lesedi Mfolo and Standw

Entelect features in the Pretoria News Workplace

Have you ever wondered why people pick, or get into, the wrong jobs? That’s something interest